At the beginning of 2026, the global corporate finance landscape underwent a tectonic shift. While MicroStrategy's move in 2020 seemed like a gamble, today holding BTC on the balance sheet is a sign of fiduciary responsibility to shareholders. As of February 2026, public companies hold over 1.12 million BTC, representing a significant portion of the market supply.

1. Why Fiat Lost: The Macroeconomic Context of 2026

By 2026, the traditional concept of "Cash is King" has fully transformed into "Cash is Trash." The main reasons:

- Financial Repression Regime: Central banks maintain interest rates below real inflation to devalue government debt. For a treasurer, holding excess cash in dollars or euros guarantees a 5–7% annual loss of purchasing power.

- The Death of the 4-Year Cycle: Contrary to the expectations of a "crypto winter," in 2026 the market shifted to structural growth, supported by steady inflows through ETFs and direct corporate purchases.

- Regulatory Clarity: The implementation of FASB rules in the United States and MiCA in Europe allows companies to report BTC on the balance sheet at market value rather than historical cost.

2. Case Studies: Market Leaders’ Strategies

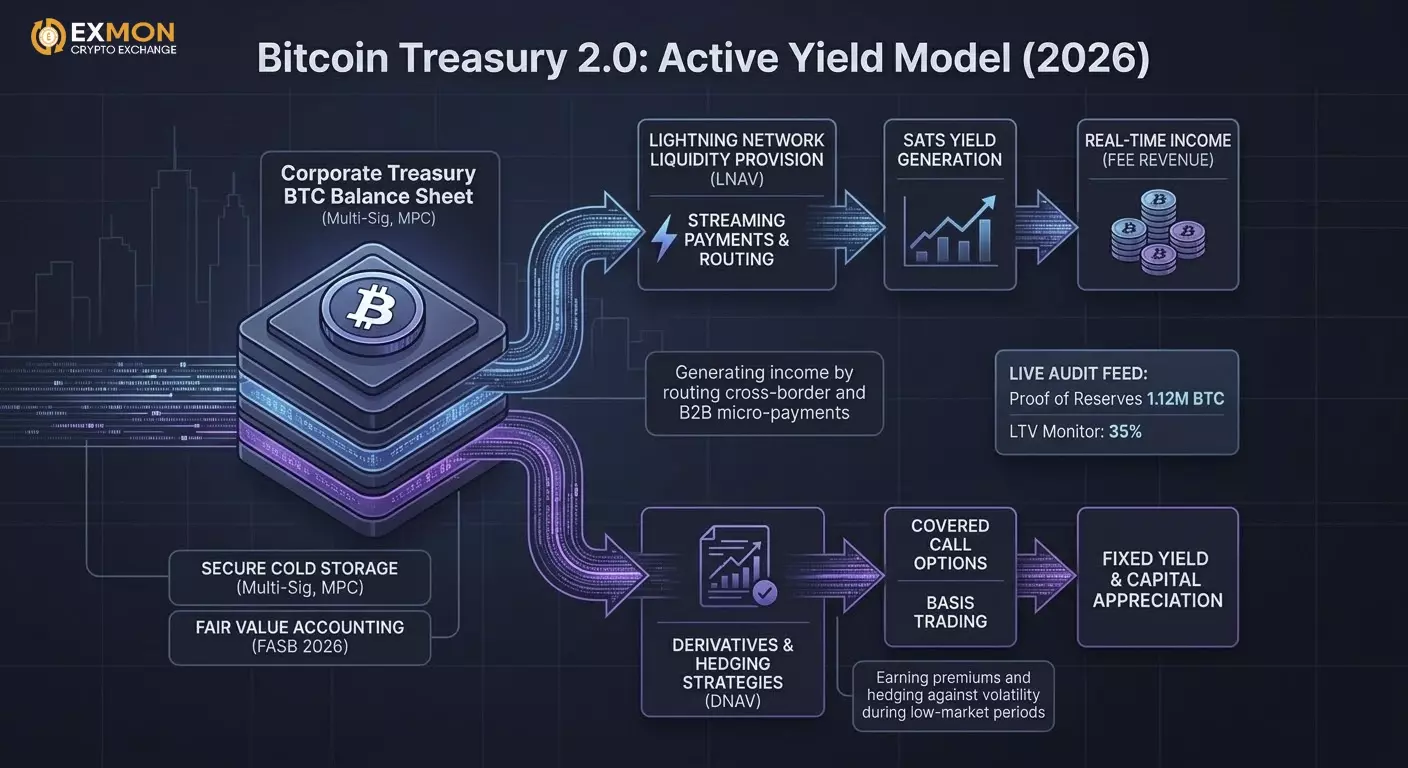

Bitcoin Treasury 1.0 Model (Passive Accumulation)

Example: MicroStrategy (now Strategy Inc.)

By February 2026, their holdings exceeded 712,000 BTC.

- Mechanics: Using cheap debt capital (convertible bonds) to purchase an asset with a scarce supply.

- Outcome: The company's shares trade with a "Bitcoin premium," effectively becoming a leveraged BTC instrument for institutional investors.

Bitcoin Treasury 2.0 Model (Active Yield)

Example: Next-generation tech companies and miners (MARA, Metaplanet).

In 2026, simply "holding" is not enough. Companies use their BTC to generate "Sats Yield."

- LNAV (Lightning NAV): Using part of the balance to provide liquidity on the Lightning Network (payment routing).

- DNAV (Derivatives NAV): Selling covered call options on a portion of the position to earn premiums in fiat or BTC during periods of low volatility.

3. Technical Implementation: How It Works Internally

By 2026, corporations no longer rely on a single Ledger or Trezor. Institutional custody and multi-signature (multi-sig) schemes have become the standard.

Storage Architecture:

- Segregated Accounts: Full legal and technical separation of client assets and custodian assets.

- MPC (Multi-Party Computation): Technology that allows transactions to be signed without collecting fragments of the private key in one place.

- Governance Policy: Software restrictions preventing fund withdrawals outside of whitelists or during nighttime hours.

4. Practical Example: Automated Buying (DCA in Python)

Many treasuries use the DCA (Dollar Cost Averaging) algorithm to minimize market impact (slippage). Here is a simplified code example for integration with a corporate broker API (for example, Coinbase Prime or Kraken):

import ccxt

import time

# Treasury strategy parameters

SYMBOL = 'BTC/USD'

MONTHLY_BUDGET = 1000000 # $1 million per month

INTERVALS_PER_MONTH = 30 * 24 # Purchases every hour

AMOUNT_PER_TRADE = MONTHLY_BUDGET / INTERVALS_PER_MONTH

exchange = ccxt.coinbaseprime({

'apiKey': 'YOUR_API_KEY',

'secret': 'YOUR_SECRET',

'passphrase': 'YOUR_PASSPHRASE',

})

def execute_treasury_buy():

try:

order = exchange.create_market_buy_order(SYMBOL, AMOUNT_PER_TRADE)

print(f"Purchase executed: {order['id']} for {AMOUNT_PER_TRADE} USD")

except Exception as e:

print(f"Execution error: {e}")

# Start accumulation loop

while True:

execute_treasury_buy()

time.sleep(3600) # Wait 1 hour

5. Lesser-Known Details and Risks of 2026

- Tax on Unrealized Gains: In some jurisdictions (for example, certain US states or EU countries), laws taxing "paper" gains from BTC are being discussed, prompting companies to relocate to more friendly zones (El Salvador, UAE, Bhutan).

- Quantum Threat: Progress in quantum computing in 2026 forces corporations to plan migration to post-quantum secure addresses, making it the top priority in security audits.

- ESG 2.0: Companies are now required to prove that their BTC is mined using renewable energy. The concept of "Green BTC" has emerged, trading at a small premium in OTC markets.

6. Tax and Accounting Breakthrough: FASB 2026 Standard

Until 2025, the main hurdle for CFOs was the "impairment" model. If BTC price fell, the company booked a loss; if it rose, profits couldn’t be recognized until the asset was sold. In 2026, the rules of the game changed decisively:

- Fair Value Accounting: Companies must now report BTC at current market value in every quarterly report. This instantly strengthens the balance sheet (Equity) during market upswings and allows BTC to be used as full collateral for fiat loans without selling the asset.

- Deferred Tax Liabilities: Large players use complex revaluation structures to minimize tax burdens during sharp price swings, spreading the tax impact over future years.

7. Liquidity and “Non-Liquidating Leverage”

One of the most innovative practices of 2026 is the use of Bitcoin-backed Loans within corporate treasuries.

Case: A manufacturing company needs $50M to buy raw materials. Instead of selling 500 BTC, it pledges them via an institutional lender (e.g., Fidelity Digital Assets or enterprise-grade DeFi protocols).

Benefits:

- No taxable event: Pledging the asset is not a sale, so Capital Gains Tax is not triggered.

- Rate arbitrage: Loan interest in dollars (e.g., 5% per year) is often lower than BTC’s historical average annual growth (>30%), effectively making the loan free over the long term.

8. Lightning Network for Corporate B2B Payments

In 2026, corporations use Bitcoin not just as a store of value (SoV) but also as a medium of exchange (MoE). Lightning Network has become the standard for cross-border payments.

- Instant settlement: Instead of waiting 3–5 days via SWIFT, treasuries process payments in 2 seconds with fees under $0.01.

- Streaming payments (Programmable Money): Companies implement micro-payments for facility rentals or API calls, deducted per second.

Example of micro-payment implementation (LND API in Python):

To automate contractor payouts on a pay-as-you-go basis, treasuries integrate with Lightning nodes:

import lnd_grpc

# Connect to the corporate node

stub = lnd_grpc.LNDClient("10.0.0.50:10009", macaroon_path="admin.macaroon")

def pay_invoice(invoice_string):

# Check treasury limits before payment

if check_compliance_limits(invoice_string):

response = stub.send_payment(payment_request=invoice_string)

print(f"Payment sent. Preimage: {response.payment_preimage.hex()}")

else:

print("Limit exceeded. CFO approval required.")

# Automatically pay invoice when a task is completed in Jira/GitHub

pay_invoice("lnbc10u1p3...")

9. Lesser-Known Aspect: “Proof of Reserves” as Trust Audit

By 2026, public companies have adopted Live Proof of Reserves. These are public dashboards showing cryptographic proof of asset holdings in real time.

- Zk-SNARKs in auditing: Zero-knowledge proofs allow a company to demonstrate it holds 10,000 BTC on its balance sheet without revealing specific addresses (UTXOs) to competitors or attackers. This protects transaction privacy while giving shareholders 100% confidence.

10. Risks and “Black Swans” of 2026

Despite institutionalization, treasurers face new challenges:

- Hard Fork Risk: Incompatible protocol upgrades require lawyers to clearly define in corporate bylaws which chain is considered the “real Bitcoin.”

- Custodian dependence: Excessive concentration of BTC with 3–4 major custodians (Coinbase, Anchorage, Fidelity) creates systemic risk. In response, top corporations adopt a hybrid model: 50% with external custodians, 50% in their own multi-sig “cold” storage.

11. Legal Engineering: Ownership Structures (SPVs and Trusts)

By 2026, major international holding companies rarely hold BTC directly on the parent company's balance sheet. Multi-layered structures are used to protect assets:

- Remote-Siloed SPV (Special Purpose Vehicles): Bitcoin reserves are placed in a separate legal entity. In case the main operating company goes bankrupt, creditors cannot claim the BTC reserve if it is designated as "protected capital."

- On-chain Governance: Company charters now include "smart contract clauses." For example, moving more than 5% of the reserve requires a digital signature (Multisig) not only from the CEO and CFO but also from an independent auditor.

12. Advanced Risk Management: Volatility Hedging

Although BTC in 2026 is less volatile than in 2020, weekly fluctuations of 10–15% are still critical for treasurers. The following tools are used to stabilize reports:

- Basis Trading (Cash-and-Carry): Buying spot BTC and simultaneously selling a futures contract of the same amount. This locks in a risk-free return (the futures premium) while keeping the asset on the balance sheet.

- Collateral Optimization: Algorithms automatically convert part of BTC into stablecoins (USDC/PYUSD) when certain "overheated market" indicators are reached and buy back when the market corrects.

13. Code Example: Collateral Health Monitoring (LTV Monitor)

If a company takes a loan backed by BTC, the treasury needs a script that monitors LTV (Loan-to-Value) in real time to avoid forced liquidation.

import requests

# Loan parameters

COLLATERAL_BTC = 500.0 # Collateral in BTC

LOAN_AMOUNT_USD = 25000000.0 # Loan of $25 million

LIQUIDATION_LTV = 0.85 # Liquidation threshold 85%

WARNING_LTV = 0.70 # Warning threshold 70%

def get_btc_price():

# Get consensus price from multiple sources (Oracle-style)

r = requests.get("https://api.binance.com/api/v3/ticker/price?symbol=BTCUSDT")

return float(r.json()['price'])

def check_treasury_status():

current_price = get_btc_price()

current_value = COLLATERAL_BTC * current_price

current_ltv = LOAN_AMOUNT_USD / current_value

print(f"Current price: ${current_price:.2f} | LTV: {current_ltv:.2%}")

if current_ltv >= LIQUIDATION_LTV:

trigger_emergency_action("IMMEDIATE_LIQUIDATION_RISK")

elif current_ltv >= WARNING_LTV:

trigger_emergency_action("MARGIN_CALL_WARNING")

def trigger_emergency_action(reason):

# Integration with corporate Slack/Telegram and auto-transfer of BTC from reserve

print(f"CRITICAL SITUATION: {reason}. Sending notification to the board of directors.")

check_treasury_status()

14. Lesser-Known Fact: "Proof of Work as a Social Filter"

By 2026, the concept of Institutional Sovereign Grade Asset emerged. Treasurers realized that Bitcoin is the only asset without "counterparty risk" at the issuance level.

- Unlike gold, which requires physical purity checks and costly logistics, or stocks, which can be diluted by additional issuance, Bitcoin is verified by code in milliseconds.

This led banks in 2026 to offer "BTC-Native Bonds" — bonds whose principal and coupons are paid strictly in satoshis, bypassing the fiat system entirely.

15. Conclusion: The New Norm

Corporate treasury in 2026 is not a choice between "risk and stability." It's a choice between a mathematically scarce asset and politically managed debt. Companies choosing Bitcoin gain:

- Global reach without borders.

- Programmable capital.

- Protection against fiat currency devaluation.

Those who ignore this shift risk ending up like "Kodak in the digital photo era": their balance sheets may look solid nominally, but their real purchasing power and competitiveness in the global market will approach zero.