Standard RSI is too basic, it just tracks the ratio of average close prices over N periods. It completely misses the big picture: rekt liquidations, Order Book Imbalance, and how fast orders hit the Time & Sales tape.

To make a momentum indicator actually map real market mechanics, we need to fuse price velocity with volume and a dynamic volatility filter (ATR). We’ll spin up a modified Z-Score Momentum combined with a volume-weighted Chande Momentum Oscillator (CMO), fully tweaked for crypto.

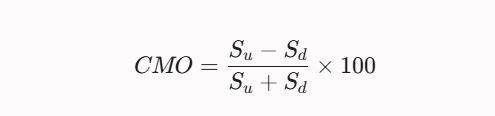

Here, S_u is the volume-weighted sum of positive close changes over the period, and S_d is the volume-weighted sum of absolute losses. This setup keeps the oscillator from getting pinned in perma-overbought territory when a pump runs on dying volume (classic divergence).

Picking the Metrics: Momentum Oscillators Compared

| Indicator / Metric | What It Actually Measures | Main Blindspot in Crypto | Pro-Trading Mod |

|---|---|---|---|

| Classic RSI | Relative strength of candle closes. | Gets completely pinned at 70+ / 30- during short squeezes. | Swap the simple moving average for a VWMA (Volume Weighted). |

| Rate of Change (ROC) | Raw price velocity (P_t - P_{t-n}). | Super choppy; highly vulnerable to noise and gaps. | Smooth it out using an EMA. |

| Z-Score Momentum | How far current momentum deviates from the expected mean. | Requires constant recalibration of the lookback window. | Use a dynamic window pegged to the volatility cycle. |

Strategy Implementation: Pine Script v5

This script fires up a Volume-Weighted Momentum Score. We are hunting for trend exhaustion by filtering extreme Z-Score prints and signal line crosses. Optimal timeframe: 15m to 1h (perfect for intraday scalping on BTC/USDT or ETH/USDT perps).

Pine Script

//@version=5

strategy("Volume-Weighted Momentum Z-Score Strategy", overlay=false, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Params

len = input.int(14, title="Momentum Period")

smooth = input.int(5, title="Signal Smoothing")

z_len = input.int(20, title="Z-Score Lookback")

upper_band = input.float(2.0, title="Overbought (Z-Score)")

lower_band = input.float(-2.0, title="Oversold (Z-Score)")

// Calc vol-weighted mom

price_change = ta.change(close)

vol_momentum = price_change * volume

// Smooth it

smoothed_mom = ta.ema(vol_momentum, len)

// Z-Score for smoothed mom

mean_mom = ta.sma(smoothed_mom, z_len)

std_mom = ta.stdev(smoothed_mom, z_len)

z_score = std_mom != 0 ? (smoothed_mom - mean_mom) / std_mom : 0.0

// Signal line

signal_line = ta.ema(z_score, smooth)

// Plotting

plot(z_score, color=color.white, title="Z-Score Momentum", linewidth=2)

plot(signal_line, color=color.yellow, title="Signal Line")

hline(upper_band, "Upper Bound", color=color.red, linestyle=hline.style_dashed)

hline(lower_band, "Lower Bound", color=color.green, linestyle=hline.style_dashed)

hline(0, "Zero Line", color=color.gray)

// Mean reversion triggers on exhaustion

long_condition = ta.crossover(z_score, lower_band) or (z_score < lower_band and ta.crossover(z_score, signal_line))

short_condition = ta.crossunder(z_score, upper_band) or (z_score > upper_band and ta.crossunder(z_score, signal_line))

if (long_condition)

strategy.entry("Long", strategy.long)

if (short_condition)

strategy.entry("Short", strategy.short)Risk Management for Momentum Trading

Aping in with a market order the exact second the signal line crosses is financial suicide. The momentum can easily catch a second wind on a cascading liquidation chain.

Instead, we enforce a strict position management framework:

- Trigger (Invalidation Point): Enter only after the candle closes and confirms the Z-Score has crossed back inside the [-2.0; 2.0] range. This proves the squeeze is running out of steam.

- Stop Loss (SL): Tie this strictly to the local extreme (the high/low of the wick that caused the squeeze) plus a 0.5 x ATR (14) buffer. If the stop is too wide, scale down your position size—never bring the stop closer.

- Take Profit (TP): Scale out in pieces. Take 50% off the table at the zero line (the momentum mean). Move the rest to break-even and let it ride to the opposite band.

- Risk-to-Reward (R:R): Minimum acceptable target is 1:2.5. Anything lower won't mathematically offset the win rate of mean-reversion models over the long run.

No oscillator can predict the future if it ignores the volume of liquidations hitting margin calls. Use Z-Score momentum as a context filter: if it’s printing extreme overbought/oversold levels, it's too late to chase the trend—it’s time to prep your reversion orders or lock in profits.