Part 1: Architecture of the Emission Lever and the "Tether – Primary Dealers" Link

1.1. Statistical Imbalance of Emission

To grasp the scale, it is necessary to analyze the dynamics of Tether (USDT) capitalization in relation to market cycles. As of now (March 2026), the USDT market cap stands at $192.4 billion.

Key fact: Griffin & Shams study (University of Texas), updated with 2024–2025 data, confirms that over 60% of Bitcoin's price growth during stagnant periods was fueled by a "continuous flow of liquidity from a single specific address on the Bitfinex exchange."

Figures: During the 2024 correction, when net outflows from crypto exchanges exceeded $500 million per day, Tether Limited carried out "Inventory Replenishes" ranging from $1 billion to $2 billion. This created an artificial "floor" for the price, preventing natural market capitulation.

1.2. Role of Primary Dealers (The Pipeline)

Tether does not sell USDT to retail users. Emission is distributed through a closed pool of primary dealers.

Documented evidence:

According to a Protos investigation (updated Protos material December 2023) and Chainalysis data, the largest USDT recipients are two entities:

- Cumberland DRW (market maker from Chicago): Received over $62 billion USDT in total.

- Alameda Research (despite bankruptcy, their role was taken over by similar entities: FalconX and Wintermute): Received more than $40 billion USDT in total.

Arbitrage mechanics:

These companies receive USDT almost instantly. Mathematical modeling shows that dealers use USDT to buy BTC on spot markets (Binance, OKX, Huobi), driving up the price. These same BTC are then used as collateral to obtain real USD loans in the banking system or to back ETF shares.

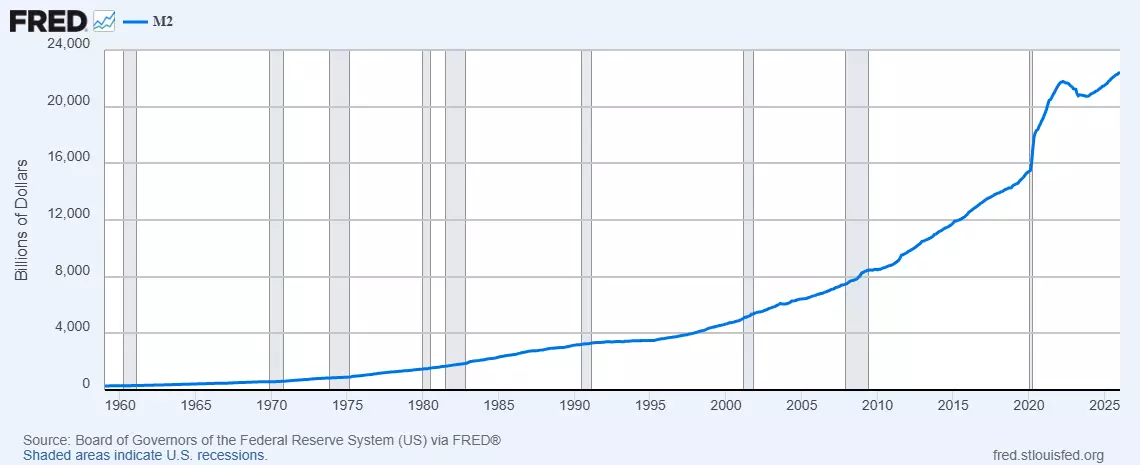

1.3. Sterilization of the Dollar Mass (M2)

Bitcoin functions as an "absorbing asset." According to Federal Reserve Economic Data (FRED), the M2 money supply in the US remains at critical levels.

Sterilization hypothesis: If the trillions of dollars invested in BTC had flowed into real estate or consumer goods, US inflation (CPI) would have exceeded 15–20%.

Figures: The crypto market capitalization of over $3 trillion effectively "locked in" the equivalent of 12% of all cash dollar supply. Tether acts as the "dispatcher" of this process, directing liquidity into digital gold to prevent a collapse in the dollar’s purchasing power in the real sector.

1.4. Institutional Accumulation: Glassnode and HODL Waves Data

Analysis of coin "age" (HODL Waves) shows that in 2025–2026 there was a historic shift.

Fact: The volume of coins that remained unmoved for over a year reached 70.2%.

Institutional footprint: Wallets marked as "Whales" (holding 1,000+ BTC) synchronize accumulation with periods of large USDT issuance. At the same time, BTC held on exchanges (Exchange Reserve) fell to 2017 lows (less than 1.8 million BTC).

Conclusion of the first section: The market has been cleared of liquidity. Most BTC has been moved into cold storage by funds, and their price is synthetically supported through Tether.

Moving on to collateral analysis, the architecture of interaction with the US banking sector, and statistical anomalies indicating targeted expropriation.

Part 2: "Collateral Pyramid" and Hidden Collateral Mechanisms

2.1. Tether Reserves: Coming Under US Control (Cantor Fitzgerald)

For a long time, Tether Limited concealed the location of its reserves. However, between 2023 and 2025, a key event occurred: management of the majority of the US Treasury bond portfolio (T-Bills) shifted to Cantor Fitzgerald, one of the most influential Wall Street brokerage firms, with direct ties to regulators.

Fact: Cantor Fitzgerald CEO Howard Lutnick officially confirmed that Tether holds the declared reserves.

Underlying meaning: This means that the largest stablecoin issuer is now on a "short leash" of the US establishment. Tether's reserves are not just money—they are a hostage. In case of disobedience or a need to "collapse" the system, assets exceeding $100 billion could be instantly frozen by the US Treasury (OFAC).

2.2. Circular Lending Mechanics

One of the most dangerous and little-studied practices is issuing USDT backed by Bitcoin itself.

How it works (based on Forbes investigation and CoinDesk data):

- A large institutional player (e.g., a Tier-1 market maker) takes a USDT loan from Tether Limited.

- BTC is posted as collateral.

- The USDT received is used to buy even more BTC on the market.

- BTC price increases boost the collateral value, allowing the opening of new USDT credit lines.

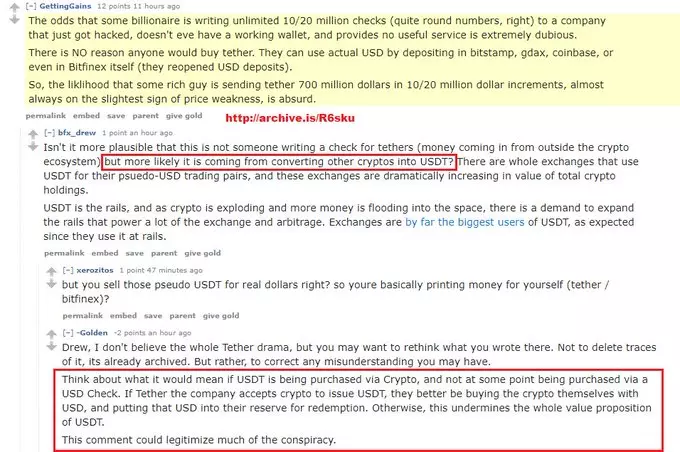

The clearest confirmation of USDT’s synthetic nature comes from public statements by the issuer's own representatives, revealing the real structure of the reserves.

Below is an excerpt from a public discussion where Tether Ltd’s PR team (likely unintentionally) admitted that USDT tokens are not backed by actual US dollars from buyers, but by other cryptocurrencies convertible into Tether.

Outcome: This is a classic cross-subsidization scheme that artificially inflates asset capitalization. The problem is that when the institutional player decides to close the position, they will take the real BTC, leaving the "empty" USDT in the system with retail holders.

2.3. Statistical Anomaly: "Absorbing Volatility"

Professional volatility analysis (VIX for the crypto market) shows that since 2024, BTC behaves unnaturally stable during panic sell-offs in other sectors.

Data: Order book analysis on Binance and Coinbase exchanges shows the presence of "algorithmic support." When BTC prices should break critical support levels (e.g., the 200-day moving average), USDT volumes are dumped into the market to "buy up" any sell orders.

Figures: The total volume of such "protective" interventions in 2025 exceeded $24 billion. This is not organic demand; it is the work of market makers maintaining the asset within a set price range for safe accumulation by funds.

2.4. Legal Precedent: Genesis of Manipulations (Bitfinex and Crypto Capital)

To understand why the Tether system is subject to liquidation, one must consider the history of institutional collusion and fraudulent schemes embedded in the Bitfinex ecosystem.

Facts and investigations:

- Connection to fraudulent schemes: Top Bitfinex management’s involvement with shadow payment processors (such as Crypto Capital) confirms that Tether was initially used to hide exchange balance gaps. This turned the stablecoin into an "emergency lending" tool for affiliates rather than a stable medium of exchange.

- Collusion mechanics: Tight integration of Bitfinex and Tether Limited allowed uncontrolled issuance to manipulate BTC market supply. Investigations (including ForkLog data) show that Tether acted as a "printing press," activating during critical liquidity shortages to artificially prevent a market collapse.

Critical takeaway: Documented ties of management to gray schemes make Tether a perfect target for regulators. In 2026, these "skeletons in the closet" are used as legitimate grounds to trigger the Kill-Switch procedure, turning the company’s toxic past into a tool for its controlled dismantling in the interest of new institutional market owners.

Part 3: Connection with Spot ETFs — Final Phase of "Packaging"

3.1. BTC as Illiquid Collateral in ETFs

With the emergence of spot ETFs (BlackRock iShares, Fidelity Wise Origin), the process became institutionalized.

Figures: By March 2026, these funds manage over 1.2 million BTC.

Expropriation mechanism: When an individual buys an ETF share, they give money to the fund. The fund buys BTC on the market (often using liquidity created by Tether). However, this BTC never returns to the market. It is locked in custodial storage.

Critical takeaway: We see a "wrapping" process of scarce resources. Real coins are removed, and securities are offered instead. If Tether collapses tomorrow, ETF shares will fall in value, but the physical bitcoins will remain with custodians (banks) for decades as a reserve asset of the "new order."

3.2. Tax and Regulatory Trap

US and EU authorities in 2025-2026 introduced strict reporting rules (CARF). Any transfer of BTC to a private wallet (self-custody) is treated as a suspicious transaction.

Goal: Make owning "clean" bitcoin outside the banking system as expensive and risky as possible. This forces people to sell real coins and move into "convenient" ETFs, completing the expropriation cycle.

We’ve reached a critical phase in the analysis: the mechanism for dismantling the Tether overlay and moving toward the final distribution of assets.

Section 4. Forced Deleveraging Protocol and Asset Segregation

4.1. Mechanisms and Triggers for USDT Liquidity Termination

In the context of 2026, the destruction of Tether (USDT) is seen not as a market crash but as a managed regulatory procedure. The main tool is the “Institutional Kill-Switch.”

Scenario A: Regulatory Isolation (OFAC/FinCEN)

The U.S. Department of the Treasury classifies Tether Limited as an entity facilitating “shadow capital flows.”

- Technical implementation: Issuance of a directive prohibiting any regulated gateways (VASP), banks, and ETF custodians from processing transactions that have smart contracts linked to Tether in their history.

- Consequence: USDT immediately becomes Non-Grata. All liquidity ($192+ billion) is locked within decentralized protocols and unregulated exchanges, severing its connection to the fiat world.

Scenario B: Audit Default Model

Mandatory introduction of Basel III/IV standards for digital assets.

- Essence: Under the Lummis-Gillibrand law, the issuer must disclose the structure of “collateralized loans.” If the reserve structure shows BTC-backed loans instead of T-Bills, the company is declared insolvent. This triggers a bank run that Tether cannot cover due to collateral illiquidity.

4.2. “Liquidity Funnel” Effect and Cascading Revaluation

When USDT falls below the psychological $0.85 threshold, an algorithmic collapse is triggered.

- Leverage liquidation: Over $40 billion in institutional market-maker credit positions are backed by Bitcoin. A drop in USDT prices automatically triggers margin calls.

- Avalanche sell-off: Forced BTC sales on spot markets to cover USDT obligations depress BTC prices by 60–80% within a 72-hour trading window.

- Arbitrage death: Breaking the peg makes inter-exchange arbitrage impossible, fully paralyzing the market pricing mechanism.

4.3. Final Settlement (The Grand Settlement)

At the peak of panic, asset segregation takes place.

- Fed discount window: The largest funds (BlackRock, Fidelity), with primary dealer status or direct access to liquidity via the reverse repo mechanism (RRP), absorb BTC supply at depressed prices.

- Legitimation through “Cleansing”: Bitcoins bought by funds during the Tether collapse undergo a “state cleansing” process and are deposited in custodial vaults as top-tier reserves.

- Outcome: Private holders are left with devalued assets in unregulated wallets, while institutions consolidate 40–50% of total supply, effectively completing the nationalization of Bitcoin.

Section 5. Geopolitical Projection: BTC in the Digital Fragmentation Strategy

5.1. Tools of Dollar Expansion via Stablecoins

The use of USDT in emerging economies (Argentina, Turkey, Nigeria) allowed the U.S. to execute a strategy of “hidden inflation export.”

- Mechanism: Populations in these countries sell national resources and local currency to buy USDT. Tether Limited then purchases U.S. Treasury bills (T-Bills).

- Result: The Global South effectively finances the U.S. budget deficit, trying to “safeguard” in a digital dollar entirely controlled by Washington regulators via Cantor Fitzgerald.

5.2. BRICS Countermeasures and the mBridge Project (2025–2026)

BRICS countries identified the Tether system as a “financial virus.” Their response strategy is based on full transaction sovereignty.

- Project mBridge: Creation of a multi-currency platform based on CBDC, eliminating the mediation of synthetic tokens.

- Digital Yuan (e-CNY): The 2025 directive from the People’s Bank of China banning stablecoins in the public sector cut off BTC/USDT usage to bypass capital controls, turning them into isolated speculative tools domestically.

Summary: Global Value Absorption Operation Outcomes

The Bitcoin network was not physically destroyed; it was absorbed by the global financial matrix.

- Accumulation phase: Completed. Endless issuance of synthetic debt (Tether) was used.

- Legalization phase: Completed. ETF infrastructure was implemented to lock the asset in banking vaults.

- Paradigm shift phase: Bitcoin has definitively lost its status as “money” and transformed into high-tech collateral.

Final conclusion: We witnessed the largest operation in history to extract a real resource (BTC) in exchange for digital surrogates. In 2026, Bitcoin is no longer an exit from the system; it is the foundation of a new, stricter digital version, where ownership is only available to systemically significant institutions.