In trading, there is a dangerous illusion: beginners look for the "holy grail" in entry points, while professionals build their careers on managing probabilities. If you risk 10% of your capital on a single trade, you are not a trader but a casino player who forgot that the house always has an edge.

Let's break down why the "magic number" of 1% is not just conservative advice but a harsh mathematical necessity.

1. The Math of Asymmetric Losses: The Recovery Trap

The main reason accounts get wiped out is the failure to understand how hard it is to recover from losses. In mathematics, this is called geometric decay.

| Loss (Drawdown) | Required Profit to Break Even |

|---|---|

| 10% | 11.1% |

| 20% | 25% |

| 50% | 100% |

| 90% | 900% |

Note: when you lose 50% of your account, you need to double the remaining balance just to get back to the starting point. Risking 1% per trade, it would take a streak of 50 consecutive losses to hit this "pit." At 10% risk, only five losing trades are enough.

2. The Law of Series and the "Gambler's Fallacy"

The market is not a coin flip, but even with a perfect strategy with a 60% win rate, streaks of 6–8 losing trades in a row are mathematically inevitable.

- With a 1% risk (considering leverage and volatility), a streak of 8 losses reduces your account by about 7.7%. Unpleasant, but psychologically manageable. You can keep trading systematically.

- With a 10% risk, after 8 losses, less than 43% of your account remains. Here comes "tilt": the urge to recover, over-sizing positions, and the inevitable margin call.

3. Position Sizing Formula (Practice)

1% risk does not mean "use 1% of your balance." It means that if the stop-loss is hit, you lose 1% of your equity.

Position sizing formula:

Example:

Account: $10,000

Risk: 1% ($100)

Instrument: BTC/USDT

Entry: $60,000, Stop-loss: $59,000 (difference $1,000)

Position size: $100 / $1,000 = 0.1 BTC.

Even if the price drops to zero, your risk is locked at the moment of entry.

4. Amygdala vs. Prefrontal Cortex Psychology

Why do people knowingly break this rule? Because of the dopamine loop. Small risk feels boring.

However, when risk exceeds a critical threshold (individual, usually 2–3%), the brain switches from analytical mode to survival mode. The amygdala shuts down logical thinking.

- At 1% risk: You can sleep peacefully; the stop-loss is just the "cost of doing business."

- At 10% risk: You refresh charts every minute. Any movement against you feels like a physical threat.

5. Automating Control (Python Example)

Professionals use scripts to remove human error from position sizing. Here's a simple function to calculate position size:

def calculate_position_size(balance, risk_percent, entry_price, stop_loss):

"""

Calculate position size to follow risk management rules.

"""

risk_amount = balance * (risk_percent / 100)

stop_distance = abs(entry_price - stop_loss)

if stop_distance == 0:

return 0

position_size = risk_amount / stop_distance

return position_size

# Example usage:

my_balance = 5000

my_risk = 1 # 1%

entry = 250.50

stop = 245.00

size = calculate_position_size(my_balance, my_risk, entry, stop)

print(f"Your ideal position size: {size:.4f} units of the asset")

6. Little-Known Fact: "The Ruin Effect" (The Ruin Theory)

In actuarial mathematics, there is a concept called Probability of Ruin. The idea is that even with a positive expected value in your strategy, if the risk per trade is too high relative to the sample size, your chance of going broke approaches 100% before the strategy can realize its advantage.

1% risk is a statistical buffer that allows you to survive until a profitable streak.

7. The Concept of "R-Multiples" and Expected Value

Professionals measure profit not in dollars or percentages of the account, but in R (risk units). If your risk per trade is 1% ($100) and you earn $300, your profit is 3R. If you hit the stop, your loss is -1R.

Why does this matter? With a 1% risk, you can be wrong 70% of the time and still stay profitable if your average Risk/Reward ratio (R:R) is 1:3.

With a 10% risk, you need an exceptional win rate, because a series of 3–4 mistakes can psychologically "break" a trader, forcing them to close profitable trades too early (out of fear of losing what’s left), destroying the expected value.

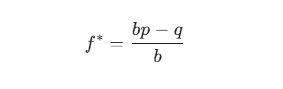

8. Lesser-Known Detail: The Kelly Criterion

There’s a formula to determine the optimal bet size — the Kelly Criterion. It’s used by professional poker players and hedge funds.

Where:![]() — fraction of capital to risk;

— fraction of capital to risk;

b — profit odds (e.g., 2 to 1);

p — probability of winning;

q — probability of losing (1 - p).

Key insight: Even if the Kelly formula tells you to risk 5% or 10%, professionals use "Fractional Kelly" (usually 1/4 or 1/10 of the formula). That’s how you get the typical 0.5%–1% risk. It’s a protection against "black swans" — market events your stats don’t account for.

9. Monte Carlo Simulation: A Glimpse into the Future

If you run your strategy through a Monte Carlo simulation (randomly shuffling the sequence of your trades), you’ll see something scary: with a 5% risk, the same strategy can make you a millionaire in one scenario and bankrupt in the first month in another due to unlucky trade order.

1% risk is the only way to keep your equity curve smooth. The lower the risk, the less "noise" and randomness affect your annual results.

10. Practical Implementation Algorithm

To stop "blowing up" your account, do the following right now:

- Set a Hard Stop at the account level: Many modern platforms allow you to block trading if daily losses exceed 3% (3 trades at 1% each).

- Forget leverage: Leverage is just a tool to make your 1% risk match the position size you need. If you need 20x leverage for a 1% stop, use it, but your actual monetary risk should remain the same.

- Position sizing table: Create a cheat sheet (or script) where each asset already has the lot size calculated for a standard stop-loss.

Example code for TradingView (Pine Script)

Add this code to your indicator to see your risk directly on the chart:

//@version=5

indicator("Risk Calculator", overlay=true)

risk_perc = input.float(1.0, "Risk % per Trade")

stop_level = input.price(0.0, "Stop Loss Price")

risk_amount = strategy.equity * (risk_perc / 100)

diff = math.abs(close - stop_level)

pos_size = diff > 0 ? risk_amount / diff : 0

plotshape(false) // Empty plot

log.info("With 1% risk, your position size is: " + str.tostring(pos_size))

Summary: Survival Is Victory

In trading, you don’t need to be the smartest, you need to be the last one standing. Those who risked 10% are already gone. Those who risk 1% will survive any market storm and catch their "bull rally."

Math is ruthless: either you follow the 1% rule, or the market will take everything. There’s no middle ground.